For most families, a home is their single biggest investment. The ups and downs of the housing market affect not only homeowners but also the broader economy. When prices rise, people often feel wealthier and spend more freely. When prices fall, spending slows and the effects ripple outward, sometimes dragging down the economy.

The US Federal Reserve System (Fed) plays a central role in stabilising the economy, partly by adjusting interest rates. However, new research suggests that what the Fed says—and how it says it—can be just as impactful as the decisions it makes.

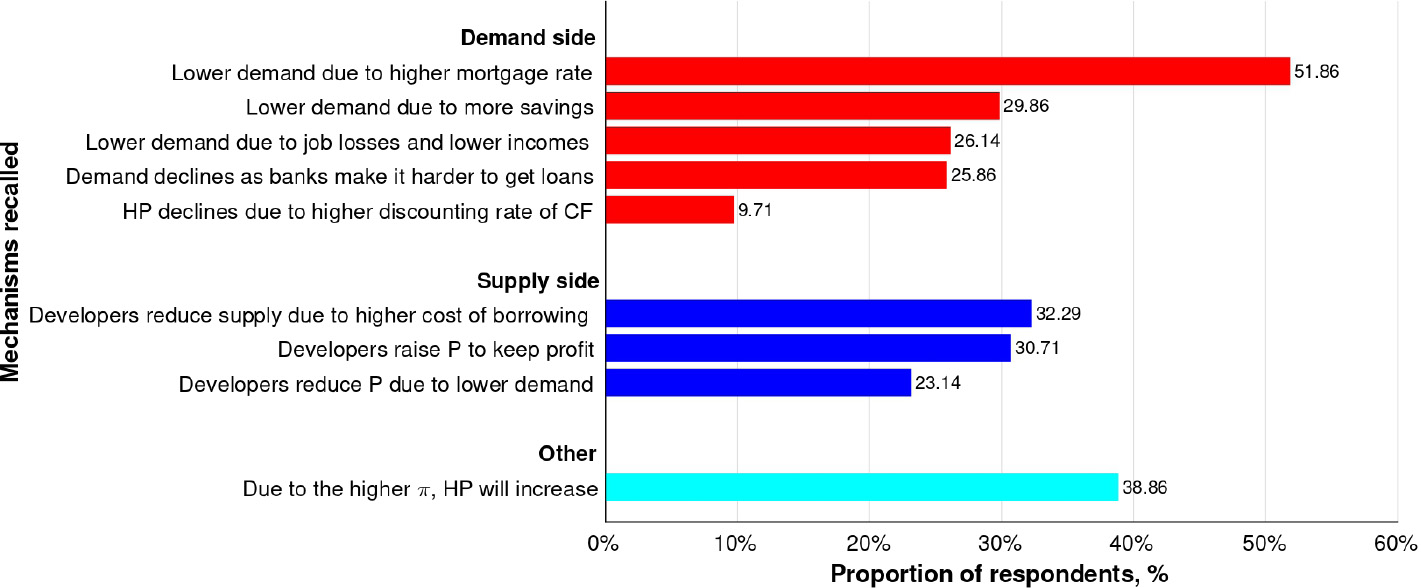

The Puzzle of Weak Reactions

House prices depend not only on supply and demand in the present but also on what people expect to happen in the future. If buyers believe that prices will continue to rise, they may rush to purchase homes, pushing prices higher. If they think prices will fall, they may wait, slowing the market. Expectations also affect decisions about renovations, selling a home, or investing in housing-related assets.

A team of economists—Kuang Pei, Carola Binder, and Tang Li—conducted large-scale online surveys between 2022 and 2025 to explore how the Fed’s communication influences American beliefs about the housing market. Their study, Central Bank Communication and House Price Expectations, published in the leading economic journal Journal of the European Economic Association, highlights both the power and the limitations of central bank messaging.

One of the most striking results was that simply telling people about current or expected interest rate changes had little impact on their average outlook for house prices. This puzzled the researchers, as interest rates are widely believed to be one of the most important factors influencing housing affordability.

How Mental Models Shape Beliefs

The explanation for this surprising finding lies in how differently people understand the housing market. Americans hold a wide range of ‘mental models’ about the relationship between interest rates and home prices. Some understand that higher rates usually mean more expensive mortgages, which tend to slow home-buying. Others either fail to make the connection or believe that other forces, such as inflation, will have a stronger impact.

When participants were given not only interest rate projections but also a simple explanation of what economists call the ‘mortgage rate mechanism’, the results changed dramatically. The explanation spelt out that higher Fed rates lead to higher mortgage rates, which discourage buyers and prompt some current owners to sell at lower prices, ultimately causing prices to fall. With this context, participants significantly revised their expectations downward, by an average of seven percentage points in one experiment. Even more strikingly, this effect persisted for some participants months later, suggesting that people were not just reacting in the moment but genuinely adjusting the way they thought about the housing market.

More Than Words: The Power of Delivery

The researchers also examined whether the way the Fed communicates affects people’s expectations. Using clips from Fed Chair Jerome Powell’s press conferences, they tested how participants reacted to different formats: the text of his remarks, the audio of his speech, and the full video including his voice and body language. The results were striking: the text alone had a modest effect, the audio produced stronger reactions, and the video had the greatest impact.

Many viewers interpreted Powell’s tone of voice and body language as signalling trouble for the economy. Interestingly, participants who already believed that rising home prices would hurt them financially often reacted to this negative impression by expecting prices to climb even higher, possibly because they feared conditions might get worse.

The Role of Personal Experience

Personal experience also played a significant role in shaping expectations. People who had recently dealt with mortgage payments, or whose family and friends were navigating the housing market, were more likely to think in terms of the mortgage rate mechanism. Their lived experiences seemed to provide a framework for connecting the dots between interest rates and housing costs.

Lessons for the Fed

The research findings have important implications for monetary policy. They suggest that Fed communication is not just a formality but a powerful policy tool. Interest rate adjustments alone do not always translate into changes in public expectations. However, when paired with clear, accessible explanations of how the adjustments affect everyday life, the Fed’s words can shift how people think about the future. The mode of delivery matters as well. Tone of voice and body language can amplify the message, sometimes more strongly than the words themselves.

The research also underscores how unevenly people interpret economic news. For some, negative signals from Fed officials suggest that housing demand will weaken, leading them to predict falling prices. For others, the same signals lead to anxiety about worsening conditions, causing them to expect prices to climb. In both cases, people’s personal circumstances and prior beliefs play a key role in shaping how they interpret what they hear.

Final Thoughts

The broader lesson is that central bankers cannot assume the public will process technical information the same way financial professionals do. To truly influence expectations, the Fed needs to communicate in plain language and explain how policy decisions connect to household finances. It also needs to be mindful of how tone and delivery can shape the message.

In housing, as in much of the economy, expectations can be as powerful as reality. The Fed’s words ripple far beyond financial markets, reaching living rooms across the country and shaping how Americans think about their most valuable asset: their homes.sical objects; they are intellectual companions that travel with him across the world, shaping the research that enriches the field of history.

About the author(s)

Kuang Pei is an associate professor of macroeconomics in the Faculty of Social Sciences at the University of Macau (UM). He obtained his PhD in economics from Goethe University Frankfurt, Germany. Prior to joining UM, Prof Kuang was an associate professor of macroeconomics and co-leader of the macroeconomics and finance research group at the University of Birmingham, UK.

Carola Binder is an associate professor of economics at the University of Texas at Austin, US. She obtained her PhD in economics from the University of California, Berkeley. She is a research associate in Monetary Economics in the US National Bureau of Economic Research, a non-resident fellow at the Brookings Institution, and a senior affiliate scholar at the Mercatus Center. Prof Binder is also a member of the Editorial Board for the American Economic Review, and an associate editor for the Review of Economics and Statistics and the Journal of Money, Credit, and Banking.

Tang Li is a lecturer of economics at the University of Reading, UK. He previously worked at the University of Essex and the University of Middlesex. Dr Tang obtained his PhD in economics from the University of Birmingham and MPhil in Economics from the University of Cambridge.

Text: Kuang Pei, Carola Binder, Tang Li

Photo: Kuang Pei, Carola Binder, Tang Li, Editorial Board

Source: UMagazine Issue 32

Academic Research is a contribution column. The views expressed are solely those of the author(s).